Likes:

Likes:

Reply With Quote

Reply With Quote

Boys-

Calm down please, let's keep things civil.

Please use your "indoor" voices now.

Thank you.

ChemEng, inflation is a fact of life.

A dollar today is worth more than a dollar 5 years from now and a dollar 5 years ago is worth more than that same dollar today.

Here's your argument: {CORRECT ME IF I'M WRONG}

If a person put $100,000 into a guaranteed 3% traditional FIXED annuity at the end of year one (1) they would have $103,000.

But your point is BECAUSE of a 4% rate of inflation the $100,000 just left alone by itself in the cookie jar is only worth $96,000 at the end of year one (1) because of the 4% inflation hence 3% growth on the $96,000 is really only worth $2,675 because 3% on $96,000 is $2,880 but with a 4% rate of inflation in terms of real dollars the value of the interest earned is only really worth $2,675.

So at the end of one year the person really doesn't have $103,000 in actual purchasing power they only have $98,675.

That's your point. Right?

So they have lost $1,325 by saving $100,000 @ 3%. Right?

That is an absurd argument.

For the 4% rate of inflation to TOTALY effect your pocketbook by 4% one would have to purchase EACH and EVERY item that went into the inflation calculation and they would have to do THAT each and every year.....year after year.

Now, let me asked another rhetorical question:

Do people buy each and every item that goes into the Consumer Price Index, i.e., houses, cars, durable goods, services, consumer appliances, clothing, etc., EACH AND EVERY YEAR?

See THIS link.

Moving on to....Immediate Annuities.

NOBODY BUYS THEM.

Period.

End of story.

UNLESS there is a compelling reason to do so, such as, to provide lifetime income for a disabled child or spouse or to SLOW DOWN MediCAID spend down for nursing home benefits or to fund a Qualified Income or Special Needs Trust for MediCAID qualifications.

When you buy an Immediate Annuity you are IRREVOCABLY trading your cash asset for the agreed upon INCOME STREAM and once that has occurred it CANNOT be undone.

That is the reason why NOBODY BUYS THEM, UNLESS there is a compelling reason to do so.

It is also the reason 99% of ALL deferred annuities and NEVER annuitized.

I didn't say people don't take a Lifetime Income Stream from deferred annuities.

I said they are almost always NEVER annuitized.

Which is why the Annuity Date provision reads:

Boys-

Calm down please, let's keep things civil.

Please use your "indoor" voices now.

Thank you.

Gary Spicuzza admits that annuities are a poor tool when inflation is figured in, but he still wants to sell them. LIkely, this is his only income and he is bound to try to meet the monthly bills by marketing this stuff. So, to admit the truth would leave him no defense for doing what he does.Originally Posted by ChemEng

He doesn't like your questions, because his own answers reveals the truth.

Annuities are just really poor tools for investment, and really expensive tools for insurance.

Chem, after reading other forum boards, we know that Gary will never give up the goods. It's just one chart after another showing the same information, and he is the only one that either cannot or will not see the truth.

Ultimately he keeps going until he gets banned from a site, which must make him feel victimized and justified, which is probably what all this really is about...

SkyPilot, before I move on to Variable Annuities, I'd like to read your intelligent comments regarding "SOME" of the earnings potential in a FIXED Indexed Annuity.

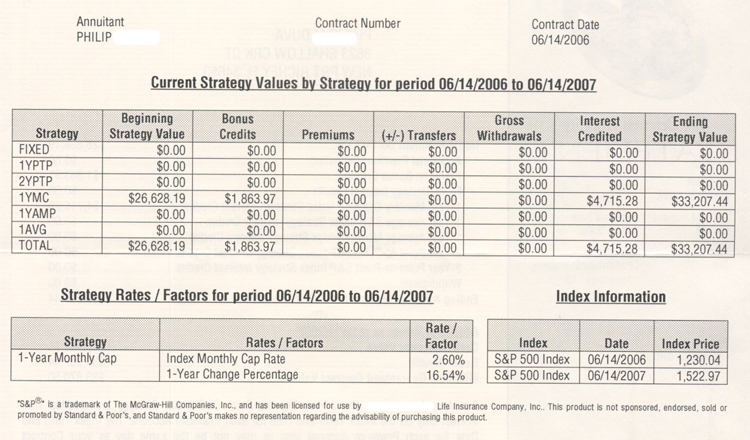

Please advise the General Public who pour billions of dollars into FIXED Indexed Annuities EACH YEAR EXACTLY what's wrong with receiving, {[strings attached], a 7% up front interest premium bonus} on their savings and then receiving an additional 16.54% interest on the entire balance after one year WITHOUT risking one penny of principal with the day traders playing stocks like a flea market swap meet.

Im not going to even respond to Gary's inflation post. Its painfully clear what his intentions are and what his education level (academic or otherwise) isn't.

FWIW-- garyspicuzza's posts on TSPTalk has just moved up to #5 on google. People need to see just how uninformed the average insurance product salesmen are.

And yet, we fed his need through our contineuos participation in this

thread. We stand tall and steadfast to correct his errors, in hopes to

achieve, what can be done with a click of our mouse. Some don't just

love feeding the animals. Some love to feed themselves, which in turn,

ultimately ends up feeding the animal anyway. Ok, I'm full ! Have fun !

I think I agree with what it is I think you said

People he is a SALESMAN tryin to make a living arn't we all? If you learned anything on this thread, this is exctly why we are here. bring on the next one!!! Attachment 3986

ChemEng, squalebear and SkyPilot:

...Foxxx News Alert...

On the TSP Talk Forums there is a forum catagory titled "Retirement Planning" and under that heading there is a sub-forum titled Annuities.

Have I posted in the wrong section?

Did you know?....

ONLY a Licensed Insurance Agent can sell an annuity upon whatever form.

The best source of information on annuities would be from someone who actually knows what they are talking about regarding specific contract provisions and more importantly it is imperative the General Public understand that a [Traditional FIXED Annuity] IS NOT THE SAME AS A [Fixed Indexed Annuity] WHICH IS NOT THE SAME AS A [Variable Annuity] AND NONE OF THE ABOVE ARE [Immediate Annuites].

...End of Foxxx News Alert...

Okay, where was I?

Yes, I remember, moving on to VARIABLE Annuites.

Now before I go off on an Internet rant on THE infamous BLOATED PIG WITH LIP STICK, known as a Variable Annuity let me say I've seen Variable Annuities that are actively managed by sharp brokers that have performed EXTREMELY well.

A Variable Annuity is an INVESTMENT in mutual funds, bonds and other stock market products then wrapped in an annuity contract. The cash value is subject to the direct upside potential of the market AND ALL the direct downside of the market.

THEY are NOT a SAFE money savings instrument like a bank CD or a U.S. Savings Bond or a Money Market account or a Traditional FIXED Annuity or a Fixed Indexed Annuity.

Variable Annuities violate the fundamental aspect of "Safety of Principal" that is inherent is ALL annuites EXCEPT VARIABLE Annuites.

Remember my statement above?

While that statement is absolutely true, Insurance Agents DO NOT sell VARIABLE Annuites.ONLY a Licensed Insurance Agent can sell an annuity upon whatever form.

Variable Annuities are sold by the securities industry Registered Representatives who HAD to obtain a Life and Annuity Insurance License to be able to sell THE infamous BLOATED PIG WITH LIP STICK, known as a Variable Annuity.

Guess who SELLS the most annuities nationwide?

Well.... it's the day traders playing stocks like a flea market swap meet with your money.

See 2007 annuity sales graphic below:

Norman, its not too often that I disagree with you, but I do (just a little)

non the less. I make a living by working for the Federal Government. My

goal in coming here is two fold. I try to improve my retirement outlook

while trying to help others. In fact, that's what makes this website so

unique. It's membership unselfishly tries to do both without asking for

anything from anybody. Even those members who eventually went on

to offer services for a fee (ie...Ebb...etc) gave freely of themselves

and there systems without asking for a thing. I do understand that this

jewel of ours is open to the public and everyone has a right to write

what they want. However, if the intent is to sell a product, create

controversy for exposure, all in the name of making a living, I believe

there are better suited websites out there to meet his need to produce

income. Of coarse, if Tom wants to charge Gary a 10% user fee for

operating a business within this domain, I certainly wouldn't blame him.

Still, he has a right to be here, to write what he wishes and respond as

he sees fit. Ultimately it's up to me, you and the other TSPtalk members

to decide if they wish to participate in this thread. Should that be their

decision, then by all means, do so with respect. (Originator Included).

Last edited by Guest2; 06-02-2008 at 10:36 PM. Reason: spelling

You got my attention with the pictures, then you lost me with the

words. I'm done, Good Luck In Your Endevors Gary, what ever they be.

Am I allowed to say sex sells?

Posting Permissions

Posting Permissions

|

S&P500 (C Fund) (delayed) (Stockcharts.com Real-time) |

DWCPF (S Fund) (delayed) (Stockcharts.com Real-time) |

EFA (I Fund) (delayed) (Stockcharts.com Real-time) |

BND (F Fund) (delayed) (Stockcharts.com Real-time) |

||

|

Yahoo Finance Realtime TSP Fund Tracking Index Quotes |

|||||

Bookmarks